According to the Innova Database, 60% of the 11,000-plus soft drinks launches recorded globally in 2010 had a health positioning of some sort. Primarily it was in terms of passive health, although over 20% of products were launched with an active health message of some kind, albeit often in association with other passive health benefits.

"Interest in health is clearly not the only factor driving soft drinks product activity, but it has become highly significant in indicating potential future market directions, both globally and regionally," Lu Ann Williams, Head of Research at Innova Market Insights reports. "While hydration and refreshment remain key to the market, many traditional soft drinks categories such as carbonates, are maturing and there is rising interest in newer, often higher-value-added lines offering additional benefits, which increasingly seem to include healthier options", she adds.

Some soft drink products have an inherently healthy image, particularly juices and water. Others are formulated for specific benefits beyond hydration, notably sports and energy drinks. Elsewhere in the mainstream market, manufacturers also continue to position products on health platforms of various kinds. There are the passive, such as sugar-free, low-calorie and natural. Then the active, such as vitamin- and mineral-fortified, added-calcium and functional, as well as those offering specific health benefits such as immune health, heart health and oral health.

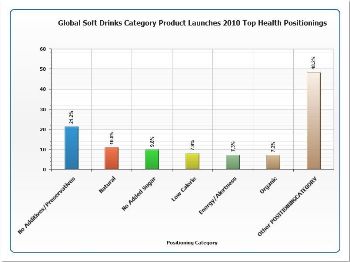

The most popular health-related claims recorded by Innova during 2010 were undoubtedly concerned with naturalness and freedom from artificial additives and preservatives. This encompassed a wide range of products, led by juices and water, which tend to be seen as inherently fairly natural. Over 20% of launches recorded by Innova were marketed as free from additives and preservatives, while well over 10% were marketed as natural. Combining the two categories resulted in nearly one-third of total soft drinks launches using either one or both claims.

The well worked health-related area of low-calorie or diet drinks also continued to receive considerable attention, with reduced-sugar, sugar-free and no-added-sugar lines taking second place overall in terms of health claims, ahead of low-calorie products. Over one-fifth of launches were positioned as either low-calorie or sugar-free/reduced-sugar/no-added sugar or both. The next place, but at a distance, went to drinks marketed as containing antioxidants, comprising about 6% of the 2010 drink product launches recorded by Innova. Just under half of these were, perhaps not surprisingly, juices and juice drinks.

In terms of active health claims, energy and alertness featured as the leading claim, reflecting the ongoing growth of the energy drinks market. Drinks using energy and alertness claims accounted for over 40% of soft drinks using any active health claims and over 8% of soft drinks launches as a whole. This type of claim overtook vitamin and mineral fortification at the head of the active health claims ranking for the first time in 2010. Sports/recovery claims remained in third place at a distance, but still seeing increased use overall through the year.

Actual energy and sports drinks accounted for nearly 7% of total soft drink launches recorded on Innova in 2010. The market for energy drinks in particular appears to have managed to maintain sales during the economic downturn, in spite of premium pricing and, or perhaps partly because of, a somewhat controversial image and some poor media publicity. It is still outperforming the soft drinks market as a whole on a global level, led by growth in Asia and Latin America. Europe is also seeing growth through ongoing product developments, including larger pack sizes, shots and flavour extensions, which are resulting in more people buying into the category. Conversely, the relatively large and developed US market is facing some difficulties in extending usage to new consumers.

For further information on the Innova Database, the representative for Australia and New Zealand is Glen Wells ([email protected]).